Battery electric vehicles (BEVs) are an important component of efforts to decarbonize transportation and achieve sustainable mobility.

by Irem Kok and Marie Rajon Bernard | International Council on Clean Transportation

Realizing the full benefits of the transition to electric vehicles hinges on establishing robust and accessible charging infrastructure networks. The challenges associated with this transition are not merely technical; they are fundamentally policy challenges. Charging infrastructure requires substantial upfront investment, coordination across multiple stakeholders, and careful policy alignment to support BEV uptake across diverse transport modes. Research by the Zero Emission Vehicles Transition Council (ZEVTC) has emphasized that timely and well-sequenced policies can promote effective charging infrastructure deployment and ensure that the transition to decarbonized transportation is just, fair, and equitable.1 Governments play an indispensable role in planning and implementing this infrastructure, yet many face uncertainty about which policies to implement and when.

While individual countries have pioneered various charging infrastructure policies, comprehensive guidance on policy sequencing and appropriate interventions for different market development stages remains limited. Policymakers require clarity on which policies are most effective during early market development or scaling phases, how policies should differ across vehicle segments, and how to help ensure that infrastructure deployment serves diverse user groups equitably. Existing policy analyses often focus on single markets or vehicle types, failing to provide the comparative, cross-sectoral perspective needed to design comprehensive charging strategies. Furthermore, countries at earlier stages of BEV adoption lack accessible frameworks that synthesize lessons from pioneering markets, leading to policies that may result in inefficiencies or inequitable outcomes.

This paper addresses this policy challenge by examining charging infrastructure policies in countries and economies around the globe and proposing a tailored policy architecture for road transportation. The analysis spans diverse transportation modes, including two- and three-wheelers, light-duty vehicles, and heavy-duty vehicles (HDVs), and considers market development phases and distinct BEV user groups. The analysis identifies common policy priorities—including addressing initial investment hurdles, promoting interoperability and user convenience, and managing integration with energy systems—while recognizing that implementation should be tailored to each transportation mode’s unique operational requirements. By providing a phase-by-phase approach with actionable policy options, this paper offers insights for policymakers to craft policies that promote effective charging infrastructure networks.

Market development framework

To analyze charging infrastructure policies across diverse contexts, this paper uses a framework that categorizes BEV market development into three stages: early market, developing market, and scaling market. This framework is conceptually inspired by Everett Rogers’ technology adoption cycle, which divides technology adopters into categories that inform our three-stage model.2

The early market phase, analogous to Roger’s “innovators” category, is characterized by initial technology introduction and limited uptake. During this phase, BEV sales typically represent less than 3%–5% of total vehicle sales, infrastructure is nascent, and adoption is driven primarily by early enthusiasts and policy mandates. The developing market phase, which corresponds to Roger’s “early adopter” and “early majority” stages, features increasing consumer interest and rapid infrastructure growth. This phase typically sees BEV sales accelerate from 3%–5% to 20%–25%. The scaling market phase encompasses the stages beyond the “chasm”—a term popularized by Geoffrey Moore to describe the gap between early and mainstream adoption—signifying a move toward widespread consumer acceptance.3 In this phase, BEV sales exceed 20%–25%, infrastructure becomes ubiquitous, and there is mass adoption of BEVs.

While conceptually aligned with the technology adoption cycle, this market development phase framework focuses on market evolution in terms of BEV sales share progression, rather than on overall stock penetration. The sales share thresholds provided above should be understood as loose illustrations rather than rigid boundaries, as the transition between phases can vary based on local conditions, vehicle segments, and policy contexts.

Based on this framework, we can classify the vehicle segments of different global markets. For instance, the current passenger car and van markets in countries like China and Norway would be classified as scaling markets. The European Union and Costa Rica may be understood as developing markets, progressing toward scaling. Meanwhile, the United States, India, Chile, and South Africa can generally be classified as early markets.

While effective policy implementation necessitates tailoring policy approaches to each transportation mode’s unique requirements, the overarching policy areas remain consistent across vehicle types during each market development phase. Understanding these common policy needs is important for creating efficient and effective charging ecosystems. The subsequent analysis demonstrates how these policy areas manifest differently across early, developing, and scaling market phases, and how implementation strategies can be adapted for distinct vehicle segments.

Furthermore, an effective charging infrastructure policy considers the diverse needs of different electric vehicle user groups, as policies designed for one group may not adequately serve another. These groups can be systematically categorized by population characteristics (urban or rural), housing situations (rented or privately owned, apartments or houses), fleet type (private or company cars, small- and medium-sized enterprises or large enterprises), and charging technology preferences (wired stationary charging, battery swapping, or wireless in-road charging). For governments seeking to promote a just and inclusive transition to electric mobility, an effective charging infrastructure strategy addresses the specific challenges and opportunities presented by each user segment.

This user-centric lens is applied throughout the policy analysis in this paper, with particular attention to promoting equitable access across income levels, housing types, and geographic locations. As markets progress from the early to scaling phases, the diversity of user groups expands, which necessitates that policies evolve to serve all segments of the BEV-adopting population.

The policies presented in this paper were selected from a diverse set of countries and economies and offer actionable insights for effective charging infrastructure deployment and market acceleration. This structured, phase-by-phase approach is designed to equip policymakers, key stakeholders (including automotive manufacturers, charge point operators, and electricity utilities), and practitioners with the tools to effectively navigate the complex transition toward electric road transportation. While this framework is applicable across all stages of market development, it may be particularly useful for countries at earlier stages of transportation electrification because it offers a clear roadmap and tested policy options. Ultimately, this framework seeks to foster enhanced collaboration, facilitate knowledge sharing, and promote the design of robust and impactful policy interventions for all countries.

Policy sequencing by market development phase

As showcased in a 2022 ZEVTC briefing paper, strategic government intervention can promote effective infrastructure deployment, especially in early market development.4 Understanding a country’s current level of technological adoption is crucial for informing the timing of policies and programs. For instance, an effective policy approach in a market with a BEV share of 2% of new registrations will drastically differ from one in a market where BEVs already constitute 60% of new registrations.

Based on an extensive literature review of global charging infrastructure policies across 15 markets in North America, Europe, Asia, and Africa—including the EU’s comprehensive Alternative Fuel Infrastructure Regulation (AFIR), the U.S. National Electric Vehicle Infrastructure (NEVI) program, India’s Faster Adoption and Manufacturing of Electric Vehicles in India, Phase II (FAME II) incentives, and innovative approaches from Canada, China, the Netherlands, Rwanda, and the United Kingdom—we identified consistent patterns in policy priorities across market phases. Although specific policy designs vary by jurisdiction and vehicle segment, the core policy challenges addressed and the types of intervention used show substantial similarity, providing a valuable, structured roadmap for policy sequencing.

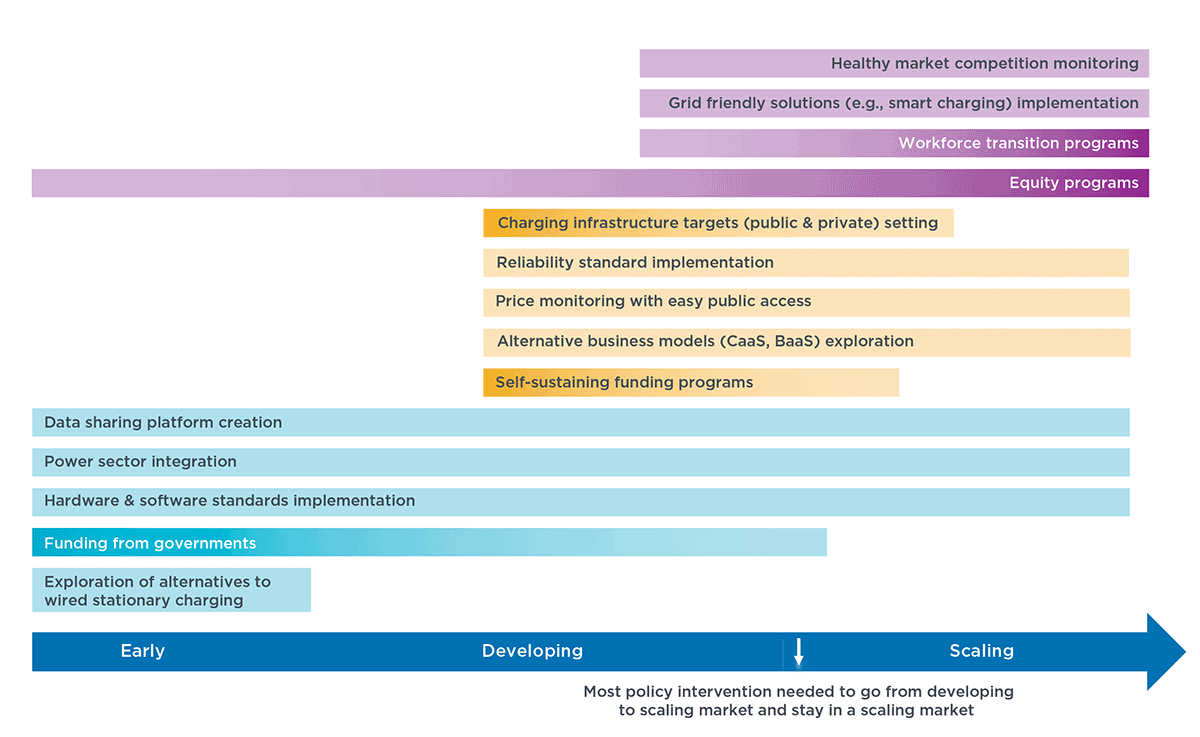

As shown in Figure 1, government intervention occurs in all market phases and across all transportation modes, but the focus of these interventions shifts. In an early market, governments typically encourage market development by providing funding for charging infrastructure deployment (from grid connection to charger purchases and installation), establishing foundational standards, and fostering cross-sector collaboration. In the developing phase, governments support the mass market adoption of EVs by setting charging infrastructure deployment targets, potentially using tenders, and developing regulations to foster user-friendly, reliable, transparent, and fairly priced charging. Lastly, in the scaling phase, government actions to promote equitable access to charging include implementing equity programs, supporting workforce adaptation, and monitoring market competition to prevent unfair pricing.

The following subsections examine each phase in detail, highlighting key policy areas and providing illustrative examples from pioneering jurisdictions. Policies are categorized by their optimal timing for implementation rather than when they were actually enacted; consequently, some policies may be listed with a phase that comes earlier or later than when the jurisdiction enacted the policy. The appendix provides

information on selected policies relevant to different BEV market development stages and road transportation modes, in addition to transferable lessons.

Early market

Policies implemented in the early market phase are foundational, aiming to kickstart the charging network and foster long-term viability by providing initial funding, setting hardware and software standards, and fostering cross-sector coordination, including through strategic grid integration.

Establishing charging infrastructure standards

Establishing charging infrastructure standards for both hardware and software in the early phase can help to ensure a cohesive market from the outset. These standards typically take two forms: (1) charging connector and communication protocols and (2) battery interoperability for swapping systems.

As the early market phase progresses, interoperability policies can foster charging options for all BEV types for both public and private charging infrastructure. The joint EU-U.S. commitment to developing the Megawatt Charging System (MCS) standard—a shared charging standard specifically for HDVs—exemplifies proactive international coordination.5 The MCS standard, endorsed by global standards bodies like IEC and ISO, aims for compatibility in both physical connectors and communication protocols, supporting international interoperability and seamless cross-border trade.

For battery swapping, standardization addresses the requirement of physical interchangeability. One example of such standards is NITI Aayog’s draft battery-swapping policy in India; this policy establishes technical standards for batteries and swapping stations to facilitate operation across different providers.6 This approach allows the market to scale while preventing proprietary lock-in that would limit consumer choice and operational flexibility.

Beyond hardware standards, smart charging mandates can be implemented in the early market phase to manage grid load. The UK’s Smart Charge Points Regulations, which includes pre-configured default charging schedules for home and workplace chargers, reflect this proactive approach to grid management.7 This policy demonstrates how governments can target private chargers for smart charging, leveraging their long dwell times for effective load shifting potential. While today’s charging infrastructure is still undergoing substantial innovation and therefore some later-stage markets like the United Kingdom are in the process of implementing smart charging policy, these mandates can be used in the early market stage to allow sufficient time for grid planning and upgrades that may be needed in the longer term, as discussed below.

Providing public funding

Public funding programs in the early stages can help to bridge the gap until market self-sufficiency is achieved. These incentives can take various forms. Some are direct financial subsidies for charging infrastructure deployment (targeting charge point operators) and for the recharging process such as free or subsidized public charging (targeting consumers). Others are funding for alternative charging solutions such as battery swapping and wireless charging. However, funding programs typically demonstrate three characteristics: diversification across use cases, targeting of specific user groups, and built-in transition mechanisms toward market sustainability.

Canada’s Zero Emission Vehicle Infrastructure Program offers distinct funding schemes tailored for public spaces, workplaces, residential buildings, fleets, and Indigenous communities.8 This segmentation recognizes that different user groups face distinct barriers and can require targeted interventions.

Enabling strategic grid integration

Grid integration is a critical consideration across all transportation modes, but it is especially important for HDVs because their high-power charging demands place a significant and concentrated strain on the electricity grid. Thus, early coordination between transportation and energy stakeholders is essential.

California’s EnergIIZE program exemplifies a strategic approach to HDV grid integration by funding both chargers and the underlying energy infrastructure and research needed to manage the high-power demand from electric trucks.9 Early engagement and adaptation within the energy sector are important due to the time required for grid upgrades and process adjustments.

Institutional coordination mechanisms can formalize early cross-sector coordination. The United State’s Joint Office of Energy and Transportation, created in 2021, leverages the combined expertise of the U.S. Department of Energy and the U.S. Department of Transportation to facilitate the alignment of infrastructure deployment with grid planning and capacity development.10 The office works to bridge institutional silos, providing technical assistance and building capacity among stakeholders, including state utility commissions that regulate the grids, to streamline sub-national implementation. Such structures enable efficient BEV grid integration and pave the way for innovative solutions like bi-directional charging to be implemented as the market matures. Early engagement across sectors can prevent the costly retrofits and deployment delays that occur when transportation and energy planning proceed independently.

Developing market

As EV markets progress beyond the early stages of adoption, the policy focus shifts from stimulating initial demand to building a robust, user-friendly, and geographically comprehensive charging network. In the developing market phase, governments can use regulatory and financial tools to promote the scale-up of charging infrastructure and support a positive user experience. Three key policy areas for this stage are: (1) setting legally binding deployment targets to drive expansion, (2) using public funds to stimulate private investment in underserved areas, and (3) implementing reliability and data-sharing standards to guarantee a seamless user experience.

Setting legally binding deployment targets

Legally binding public and private charging infrastructure deployment targets support widespread charging development on par with BEV uptake. Deployment targets balance two objectives: ensuring total charging capacity scales with fleet growth and guaranteeing geographic coverage to eliminate range anxiety and enable long-distance travel. The most sophisticated policies employ dual approaches that address both dimensions simultaneously.

The European Union’s AFIR exemplifies this dual approach for passenger cars and vans through fleet-based and distance-based targets.11 The fleet-based target mandates that the Member States ensure a total public charging power output of at least 1.3 kW for each registered BEV and 0.8 kW per registered plug-in hybrid electric vehicle, so that overall capacity grows with EV adoption. Complementing this, distance-based targets mandate the installation of fast-charging pools every 60 km along major EU transport corridors. This dual approach aims to ensure total capacity scales with EV uptake while guaranteeing geographical coverage and minimum service levels.

For HDVs, the AFIR sets progressively tighter requirements for the deployment of high-power charging stations, starting with a minimum total aggregated power of 1,400 kW every 120 km along the core Trans-European Transport Network by the end of 2025 and increasing coverage and power over time at urban nodes and safe parking areas through 2030. By setting binding, distance-based targets for public charging along key corridors, the AFIR provides the investment certainty necessary for private capital to flow into heavy-duty charging infrastructure despite longer payback periods and higher capital costs compared with light-duty charging, helping to provide comprehensive network coverage across vehicle segments.

Directing public investment to underserved areas

Even with binding targets, market forces alone often fail to deliver equitable geographic coverage, as private operators naturally gravitate toward high-traffic, profitable locations. Strategic public investment can help ensure that charging networks serve both commercially attractive urban centers and less profitable rural or low-traffic areas. Two effective approaches that have been taken by governments are competitive tenders with coverage obligations and targeted funding programs with explicit geographic equity criteria.

Germany’s Deutschlandnetz program, for example, uses competitive tenders to award contracts for building and operating 9,000 fast-charging points. This design includes coverage requirements in less profitable rural locations, supporting comprehensive national coverage.12

India’s PM E-DRIVE initiative illustrates a targeted funding approach.13 With a dedicated ₹20 billion in funding (roughly $240 million in U.S. dollars), the framework aims to expand the national network by strategically targeting both urban charging density and inter-city highway connectivity. This dual focus recognizes that comprehensive networks require both destination charging (where vehicles park for extended periods) and en-route charging (to enable travel between cities). By explicitly targeting both dimensions with dedicated funding, PM E-Drive addresses the chicken-and-egg problem where consumers hesitate to purchase BEVs due to inadequate infrastructure while operators hesitate to invest due to insufficient vehicle populations.

Implementing reliability and data-sharing standards

Having chargers on the ground is an important first step, but maintaining the good functioning of the chargers is equally important, because infrastructure availability means little if chargers are frequently broken or if users cannot easily locate, access, and pay for charging services. In the developing market phase, reliability standards with enforcement mechanisms can be implemented in addition to data-sharing requirements that enable user-friendly experiences.

The UK’s Public Charge Point Regulations, implemented in 2023, set a stringent 99% uptime requirement for direct current (DC) fast chargers (50 kW or above) to help ensure charger reliability and performance.14 Enforcement for this regulation relies on annual operator reporting using the standardized Open Charge Point Interface protocol, with potential penalties for non-compliance. This approach creates clear performance expectations while leveraging standardized data formats that reduce reporting burdens.

Data sharing can prevent fragmented information across multiple proprietary networks, which creates friction that deters adoption. Transparent data access is key for properly planning for charging infrastructure, and seamless access to information on charger locations, real-time availability, pricing, and payment options can help to provide a user-friendly charging experience. The EU’s AFIR addresses this by requiring operators to share both static and dynamic data, including availability and price information, with newly established National Access Points. These centralized repositories facilitate standardized data exchange across the EU, enabling value-added services and improving user experience. While this regulatory approach is highly viable in jurisdictions with strong centralized rulemaking, the necessity of transparent data access is universal for building consumer confidence and enabling a functional, integrated charging system.

Ultimately, the developing market phase represents a critical transition: from early-stage experimentation to systematic deployment and from government-funded demonstrations to private sector delivery. This phase can be helped by policies that build a user-friendly, reliable, and data-driven charging network capable of supporting a rapidly growing BEV fleet.

Scaling market

As BEV markets transition into the scaling phase, the primary policy focus broadens significantly. With widespread deployment underway, the government’s role can shift from incentivizing EV adoption and baseline charging network coverage to managing the long-term impacts of the shift and prioritizing sustainability, inclusivity, and healthy functioning of the charging ecosystem. Guaranteeing equitable access to charging for all residents involves supporting the workforce transition in related industries and fostering a competitive and transparent charging market. Three policy areas in this phase are: (1) implementing comprehensive equity programs to prevent charging deserts, (2) facilitating just workforce transitions in affected industries, and (3) fostering competitive markets with transparent pricing.

Implementing comprehensive equity programs

As BEV markets mature, the risk emerges that electrification benefits accrue primarily to affluent, urban populations while underserved communities—rural areas, lower-income neighborhoods, and renters without home charging access—are left behind. In a scaling market, the policy focus is ideally shifted toward ensuring that the benefits of electric mobility are accessible to all segments of society, preventing “charging deserts” in underserved communities and guaranteeing equitable access for all users.

Initiatives like California Senate Bill 1000 exemplify proactive approaches to equitable charging deployment.15 This bill requires the California Energy Commission to assess charging infrastructure deployment against demographic and income data. The assessment analyzes metrics—such as drive time to the nearest fast charger—across different communities. The findings of such assessments can then directly inform investment decisions so that funding is targeted to bridge equity gaps. By embedding equity analysis into the policy process rather than treating it as an afterthought, the framework aims to ensure that infrastructure expansion serves all communities rather than following purely market-driven patterns that can replicate existing inequalities.

China’s Tackling Areas of Weakness program demonstrates a complementary geographic approach. This program identifies and provides dedicated funding to the counties with lagging EV charging infrastructure deployment. This county-level targeting recognizes that national or provincial averages can mask significant local gaps, and that rural and remote areas require explicit attention to prevent permanent infrastructure divides. By focusing on these “areas of weakness,” the program thus promotes a more comprehensive and equitable EV charging infrastructure network.16

Supporting just workforce transitions

As the BEV market scales, supporting a just workforce transition is equally important. The shift to electric mobility will impact traditional automotive and energy sector jobs and thus necessitate proactive measures to support workforce adaptation. Some traditional automotive jobs will decline—particularly in internal combustion engine production and maintenance—while new roles in battery manufacturing, charging infrastructure installation, and electric powertrain maintenance will expand. Proactive workforce policies are essential to provide affected workers with pathways to new opportunities rather than leaving them displaced.

The EV Infrastructure Training Program (EVITP) in the United States provides a model for skill development in the emerging charging infrastructure sector. Although not a direct government program, its curriculum was developed collaboratively with a wide range of stakeholders, including auto industry, utilities, and educational bodies. The program offers comprehensive, certified training programs that prepare electricians to install and maintain EV charging equipment, directly addressing the skills gap in the growing EV sector.17 Government programs, such as the NEVI program and state initiatives like those in California, often incentivize or require the use of industry-recognized training to ensure consistent quality and support workforce adaptation.

National certification programs ensure consistent quality standards across providers while providing workers with portable credentials recognized by employers nationwide.

Beyond training programs, initiatives like incentives for companies to invest in regular workforce training and university curricula aligned with evolving needs can facilitate a smooth and equitable transition. Just transition frameworks recognize that while aggregate employment may remain stable or grow, individual workers face significant adjustment costs. Policies that smooth these transitions—through training subsidies, wage insurance during retraining periods, and placement services—enable electrification benefits to be broadly shared rather than creating winners and losers.

Fostering competitive markets

As the EV market grows, a few dominant players in the charging infrastructure space may emerge with significant market power, particularly in specific geographic areas or along key corridors. Without regulatory oversight, this concentration can lead to unfair pricing, reduced service quality, and barriers to entry that prevent new competitors from challenging incumbents. Hence, governments play a crucial role in fostering healthy market competition and transparent pricing.

Competition agencies, such those in the European Union, are increasingly monitoring the BEV charging market to identify and address potential anti-competitive practices, including abuse of local market power, market tipping, and vertical integration, all of which can limit market access.18 The findings from these analyses inform regulatory interventions before significant issues fully materialize, helping to maintain a competitive landscape and uphold fair and transparent pricing for BEV charging.

Tailored policies for different transportation modes

While overarching charging infrastructure policies provide a foundational framework, achieving effective charging infrastructure deployment requires tailored approaches that acknowledge the unique operational characteristics and needs of different vehicle segments. Two- and three-wheelers, passenger cars and vans, and buses and HDVs each have distinct charging requirements and usage patterns, and a one-size-fits-all policy strategy is insufficient to unlock the full potential of electric mobility for all vehicle segments. More specifically, vehicle segments differ in typical daily distance traveled, dwell time patterns, charging location preferences, and power requirements. Therefore, specific interventions are necessary to optimize charging solutions for each transportation mode.

The following subsections examine policy approaches optimized for each transportation mode, highlighting how the general policy priorities outlined in the sequencing framework manifest differently across segments.

Two- and three-wheelers

The electrification of two- and three-wheelers requires a mix of charging policies tailored to the segment’s diverse applications. Personal mobility applications can benefit most from low-cost stationary charging. Small battery capacities (typically 2–5 kWh) enable full overnight charging from standard household outlets, eliminating the need for dedicated charging infrastructure in many cases. India’s FAME II program prioritizes deployment of affordable AC slow chargers, which are well-suited for this application.19 This approach minimizes both user costs and infrastructure investment requirements while serving the majority of personal two-wheeler owners who park vehicles at home overnight.

Commercial applications—particularly food delivery or taxi services—present contrasting requirements. These vehicles operate on tight schedules, making traditional plug-in charging impractical. Battery-swapping and battery-as-a-service (BaaS) emerge as particularly effective solutions. For example, through government incentives, Taipei in the Taiwan province of China has built a dense network of battery-swapping stations to support its growing electric scooter fleet, demonstrating how this model enables intensive commercial use.20 Similarly, Rwanda’s supportive policy environment through its National Sustainable Mobility Policy has enabled the BaaS model for electric motorcycle taxis, lowering upfront costs and maximizing vehicle availability.21

Policies for this segment therefore require flexible strategies for personal and commercial use. Policymakers could adopt distinct solutions—such as low-cost stationary charging and BaaS models—to match each group’s unique operational demands and accelerate the electrification of two- and three-wheelers.

Passenger cars and vans

In terms of passenger cars, our analysis indicated that policies prioritizing the convenience and accessibility of charging, particularly at homes and workplaces, is of central importance. This is largely due to the fact that most passenger car charging is expected to occur at private locations.22 Policies therefore can support improving access to private charging while aiming to ensure that strategic public charging networks address gaps for long-distance travel and users without home charging access.

Two primary barriers to enabling private charging at scale are technical obstacles in multi-unit dwellings and regulatory or financial constraints on installation. Multi-unit dwellings present particular challenges, as shared electrical infrastructure, split incentives between landlords and tenants, and complex approval processes often prevent charger installation even when technically feasible.23

France’s national decree offers a model for addressing the financial barrier. By enabling the utility Enedis to prefinance electrical upgrades in apartment buildings, this

decree allows the utility to recoup costs through a fixed price for EV owners installing chargers, thereby facilitating charging at multi-unit dwellings.24 The EU’s Energy Performance Building Directive further promotes private charging by mandating pre-cabling in new residential buildings, requiring charging points, and emphasizing interoperability and smart charging features, including the “right to plug.”25 Together, these policies address barriers to private charging for both new construction and existing buildings.

Public charging networks have two distinct functions: enabling long-distance travel through corridor fast-charging and providing access for drivers without home or workplace charging options (e.g., renters, apartment dwellers, on-street parkers).

Effective public charging policy must therefore ensure both sufficient corridor coverage to eliminate range anxiety and adequate urban charging density to serve those dependent on public infrastructure.

Technical standards can promote seamless user experiences across public charging networks. The NEVI program in the United States mandates software interoperability across key areas like vehicle-to-charger communication and payment methods to facilitate a seamless user experience.26 While this mandate applies to government-funded chargers and deployment remains in its early stages, this standardization can help to transform public charging from a collection of incompatible proprietary networks into an integrated system comparable to the gasoline station experience.

Finally, policies supporting proactive grid planning and streamlined utility permitting can complement these efforts. Policies like the Netherlands’ National Grid Congestion Action Programme support the widespread deployment of charging infrastructure through anticipatory grid planning that uses forecasts of future electricity demand to identify and schedule necessary grid infrastructure upgrades.27 Programs such as this represent a shift away from a reactive approach, thereby helping grid capacity keep pace with the growing demand from EV charging. Smart charging regulations like the United Kingdom’s Smart Charge Point Regulations can optimize charging times and grid integration, particularly in residential settings where vehicles are parked for extended periods.

Ultimately, an effective charging strategy for passenger cars and vans involves removing private charging barriers, establishing strategic public networks, and implementing proactive grid planning.

Buses and heavy-duty vehicles

Heavy-duty vehicles require a dedicated charging strategy to meet their unique physical characteristics and energy demands, as well as their diverse operational patterns. Charging for HDVs necessitates larger parking spaces, higher-power connections—which can place significant strain on the grid—and strategic locations that align with freight logistics rather than passenger travel patterns. The energy demand from trucks is also highly concentrated, primarily occurring at depots, key industrial areas, and along the major freight corridors that connect them.

The most cost-effective and grid-friendly approach for many HDV fleets, especially those with return-to-base operations, is low-power overnight depot charging. Utilizing long dwell times for slower charging minimizes electricity costs, reduces the need for expensive grid upgrades, and enables managed charging to align with periods of high renewable energy generation.

When depot charging is not sufficient, particularly for regional and long-haul applications that require charging mid-route, a public network along strategic freight corridors becomes essential. Unlike passenger cars, where corridors primarily serve occasional long-distance travel, HDV corridors serve regular freight routes with predictable patterns. This concentration enables strategic, targeted deployment rather than comprehensive coverage: focusing infrastructure investment on major freight corridors can produce substantially higher utilization and faster payback than dispersed deployment.

Policies like the EU’s AFIR, which sets binding distance-based targets for high-power HDV stations, and the U.S. National Zero-Emission Freight Corridor Strategy,28 which provides a phased roadmap and strategic guidance for infrastructure alignment, are both designed to help build this foundational network. These frameworks provide investment certainty and a baseline of coverage to support the market’s development by mandating or signaling the deployment of high-power charging stations at specified intervals along key routes.

While existing high-power chargers (up to 350 kW) can serve many needs, megawatt-level charging standards—like the EU-U.S. joint commitment to the MCS standard—can enable the most demanding, high-mileage trucks to refuel during mandatory driver breaks. This makes electric powertrains viable for long-haul operations where depot charging alone is insufficient.

However, deploying megawatt-level charging at scale presents hurdles, including high infrastructure costs and strain on local electricity grids. To address these challenges, some markets are exploring alternative solutions. In China, battery swapping for HDVs has been deployed at scale, driven by national pilot programs that target specific high-use applications where minimizing downtime is paramount like heavy-duty tractors

at ports, mining trucks, and urban construction vehicles.29 Meanwhile, Sweden’s REEL project analyzes the optimal mix of depot charging and opportunity charging coupled with charging management systems and grid integration planning.30 These examples underscore that a successful HDV charging strategy can rely on a tailored mix of solutions: prioritizing cost-effective depot charging wherever possible, building a strategic corridor network, and carefully planning for the grid integration of high-power technologies.

In conclusion, the policy examples presented underscore how charging infrastructure policies can be tailored to the specific characteristics of each transportation mode. From affordable slow-charging and battery swapping for two- and three-wheeler commercial fleets, to increased home, workplace, and public charging for passenger cars, depot-charging, battery swapping, and strategic corridor development for HDVs, targeted policy interventions can unlock the full potential of electric mobility across the road transportation landscape…

Conclusion

The global transition to EVs is essential for meeting climate goals and adopting sustainable transportation, and charging infrastructure deployment will play a key role in determining whether this transition succeeds or stalls. Deploying effective charging infrastructure is a policy challenge that requires careful planning and consideration

of multiple interconnected factors. This paper addresses this challenge by providing a structured policy framework that sequences interventions according to market maturity, tailors the approach to individual vehicle segments, and embeds equity considerations throughout. Three core insights emerge from our global policy review.

First, effective charging infrastructure policy is guided by the stage of market development. The prevailing market phase—early, developing, or scaling—is the most important determinant of policy priorities. While vehicle type and country-specific contexts require policy adaptations, the overarching policy framework benefits from dynamic sequencing to align with the maturity of the EV market. Early markets require foundational investment in standards, catalytic public funding, and cross-sector collaboration to establish viable infrastructure. Developing markets benefit from binding deployment targets, strategic gap-filling through tenders, and user-friendly, reliable, transparent and fairly priced charging through regulation. Lastly, scaling markets necessitate equity programs addressing systemic access disparities, workforce transition support, and competition oversight to prevent market consolidation.

In this sequence, policies are layered and cumulative; foundational support from the early market remains essential to enable the more complex regulations required as the market matures. This phased approach helps ensure that government interventions are not only timely and relevant but also progressively targeted to address the most pressing challenges and opportunities at each market stage. This maximizes the impact of public resources and fosters a sustainable trajectory for electric mobility.

Second, effective implementation of the phased policy framework involves tailoring policies to the unique needs of different vehicle segments. While broad policy categories provide a common foundation, the diverse operational characteristics and charging requirements of two- and three-wheelers, passenger cars and vans, and HDVs require distinct policy instruments in conjunction with the phased approach.

For instance, for two- and three-wheelers, particularly in price-sensitive early markets, the framework points toward policies that address personal and commercial use separately. Policies could support cost-effective, slow AC charging solutions for homes and depots while enabling innovative business models like battery-as-a-service for high-use commercial fleets. For passenger cars and vans, which are predominantly charged at private locations, a successful approach to implementation might involve policies that remove barriers to home and workplace charging, such as grants for workplace charging, “right-to-plug” laws, and incentives for pre-cabling in buildings.

This strategy requires removing private charging barriers, establishing strategic public networks, and implementing proactive grid planning to keep pace with BEV adoption. Finally, for HDVs, where distinct operational needs require a range of charging solutions, applying the phased approach can involve prioritizing depot charging, strategic corridor development, and robust grid integration. High-power charging standards and battery swapping can also play a role, particularly in the scaling phase, in meeting the stringent demands of long-haul segments that require rapid recharging. This vehicle-specific differentiation is essential for addressing the unique challenges and unlocking the specific electrification potential of each transportation segment.

Third, a successful transition to electric mobility hinges on a user-centric and equitable policy paradigm within the policy framework from the outset. Effective charging infrastructure strategies extend beyond technological and economic considerations to actively address the diverse needs and circumstances of all potential EV users across all market phases. By categorizing users by population density, housing type, and fleet characteristics, policymakers can identify and overcome distinct accessibility challenges. The analysis shows that intentionally designed policies—such as targeted funding for underserved communities, “right-to-plug” laws for renters, and support for diverse business models—can prevent “charging deserts” and ensure that the benefits of electric mobility are broadly distributed across all segments of society. This proactive focus on equity from the early market stage onward is fundamental for achieving a truly just and inclusive transition for all.

The proposed phased approach elucidated in this paper, coupled with vehicle-specific tailoring and a user-centric equity lens, provides a comprehensive framework that can be used to design effective and future-oriented policies. As BEV markets continue to evolve and mature, ongoing policy adaptation and innovation are important for addressing emerging challenges and capitalizing on new opportunities. This includes continuous monitoring of market dynamics, technological advancements, and societal impacts, as well as fostering ongoing dialogue and collaboration among governments, industry stakeholders, and user communities. This framework provides a structured approach to help ensure that charging infrastructure deployment is timely, targeted, and equitable—enabling EVs to deliver their full climate and social benefits across all transportation segments and user populations.

References

1 Marie Rajon Bernard et al., Deploying Charging Infrastructure to Support an Accelerated Transition to Zero-Emission Vehicles (International Council on Clean Transportation, 2022), https://zevtc.org/deploying charging-infrastructure-sep22/.

2 Everett M. Rogers, Diffusion of Innovations, 5th ed. (Free Press, 2003).

3 Geoffrey Moore, Crossing the Chasm: Marketing and Selling Disprutive Products to Mainstream Customers (Harper Business Essentials, 1991).

4 Rajon Bernard et al., Deploying Charging Infrastructure.

5 European Commission, Joint Statement EU-US Trade and Technology Council of 31 May 2023 in Lulea, Sweden, May 31, 2023, https://ec.europa.eu/commission/presscorner/detail/en/statement_23_2992.

6 NITI Aayog, Draft Battery Swapping Policy, April 20, 2022, https://www.niti.gov.in/sites/default/ f iles/2023-03/20220420_Battery_Swapping_Policy_Draft_0.pdf.

7 The Electric Vehicles (Smart Charge Points) Regulations, SI 2021/1467 (United Kingdom), https://www.legislation.gov.uk/uksi/2021/1467/contents/made.

8 “Zero Emission Vehicle Infrastructure Program (ZEVIP),” Government of Canada, updated October 25, 2025, https://natural-resources.canada.ca/energy-efficiency/transportation-alternative-fuels/zero emission-vehicle-infrastructure-program/21876

9 “About,” EnergIIZE Commerical Vehicles, accessed October 31, 2025, https://www.energiize.org/about.

10 “About,” Joint Office of Energy and Transportation, accessed October 31, 2025, https://driveelectric.gov/ about.

11 Regulation (EU) 2023/1804 of the European Parliament and of the Council 13 September 2023 on the deployment of alternative fuels infrastructure, and repealing Directive 2014/94/EU (Text with EEA Relevance), OJ L 234, 1–47 (2023), https://eur-lex.europa.eu/legal-content/EN/ TXT/?uri=CELEX%3A32023R1804

12 “The Deutschlandnetz,” The National Centre for Charging Infrastructure, accessed on March 21, 2025, https://nationale-leitstelle.de/en/deutschlandnetz/.

13 Ministry of Heavy Industries, “India Accelerates National EV Charging Grid under PM E-Drive,” press release, May 21, 2025, https://www.pib.gov.in/PressReleasePage.aspx?PRID=2130225#:~:text=With%20 a%20financial%20outlay%20of,charging%20stations%20across%20the%20country.

14 The Public Charge Point Regulations, SI 2023/1168 (United Kingdom), https://www.legislation.gov.uk/ uksi/2023/1168/contents/made.

15 “Electric Vehicle Infrastructure Deployment Assessment – SB 1000,” California Energy Commission, accessed November 5, 2025, https://www.energy.ca.gov/programs-and-topics/programs/clean transportation-program/electric-vehicle-infrastructure.

16 Ministry of Finance, Ministry of Industry and Information Technology, and Ministry of Transport, [Notice on the pilot work of county-level charging and exchange facilities to make up for short boards], April 9, 2024, https://www.gov.cn/zhengce/zhengceku/202404/ content_6945040.htm.

17 “About Us,” Electric Vehicle Infrastructure Training Program (EVITP), accessed on March 21, 2025, https:// evitp.org/about-us/.

18 European Commission, Competition Analysis of the Electric Vehicle Recharging Market across the EU27 + the UK (Publications Office of the European Union, 2023), https://op.europa.eu/en/publication-detail/-/ publication/c9f5b4eb-72ee-11ee-9220-01aa75ed71a1.

19 Sumati Kohli, Electric Vehicle Demand Incentives in FAME II Scheme and Considerations for the Next Phase (International Council on Clean Transportation, 2024), https://theicct.org/publication/electric-vehicle demand-incentives-in-india-the-fame-ii-scheme-and-considerations-for-a-potential-next-phase-june24/.

20 Asian Development Bank, Electric Motorcycle Charging Infrastructure Road Map for Indonesia, 2022, https://www.adb.org/sites/default/files/publication/830831/electric-motorcycle-charging-infrastructure indonesia.pdf. 21 Cheng Zhang and Hong Miao, Solar-Powered Battery Swap Stations Could Speed Rwanda’s Shift to Electric ‘Motos’ (World Resources Institute, March 25, 2024), https://www.wri.org/insights/solar-powered-battery swap-stations-rwanda-shift-electric-motos.

22 Logan Pierce and Peter Slowik, Home Charging Access and the Implications for Charging Infrastructure Costs in the United States (International Council on Clean Transportation, 2023), https://theicct.org/ publication/home-charging-infrastructure-costs-mar23/. 23 Alexander Tankou et al., Policies and Innovative Approaches to Maximizing Overnight Charging in Multi Unit Dwellings (International Council on Clean Transportation, December 21, 2023), https://theicct.org/ publication/izeva-maximizing-overnight-charging-in-multi-unit-dwellings-dec23/.

24 Délibération de la CRE du 12 Avril 2023 Portant Proposition sur l’Encadrement de la Contribution Prévue par le Décret n° 2022-1249 du 21 Septembre 2022 Relatif au Déploiement d’Infrastructures Collectives de Recharge Relevant du Réseau Public de Distribution dans les Immeubles Collectifs à Usage Principal d’Habitation [Deliberation of the CRE of April 12, 2023 on a proposal on the framework of the contribution provided for by Decree No. 2022-1249 of September 21, 2022 on the deployment of collective charging infrastructures under the public distribution network in collective buildings for main residential use], Deliberation 2023-103, April 12, 2023, https://www.cre.fr/documents/deliberations/encadrement-de la-contribution-prevue-par-le-decret-n-2022-1249-du-21-septembre-2022-relatif-au-deploiement-d infrastructures-collectives-de-recha.html

25 Directive (EU) 2024/1275 of the European Parliament and of the Council of 24 April 2024 on the Energy Performance of Buildings (recast) (Text with EEA relevance), OJ L 2024/1275, May 8, 2024, https://eur-lex. europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32024L1275.

26 “National Electric Vehicle Infrastructure (NEVI) Formula Program,” United States Department of Energy, accessed October 6, 2025, https://afdc.energy.gov/laws/12744.

27 Zsuzsanna Pató, Gridlock in the Netherlands (Regulatory Assistance Project, 2024), https://www.raponline. org/wp-content/uploads/2024/01/RAP-Pato-Netherlands-gridlock-2024.pdf

28 Joint Office of Energy and Transportation, The National Zero-Emission Freight Corridor Strategy, March 2024, https://driveelectric.gov/files/zef-corridor-strategy.pdf.

29 Hongyang Cui et al., China is Propelling its Electric Truck Market by Embracing Battery Swapping (International Council on Clean Transportation, 2024), https://theicct.org/china-is-propelling-its-electric truck-market-aug23/.

30 Closer, REEL Regional Electrified Logistics: Charging Infrastructure for Trucks, 2024, https://closer. lindholmen.se/sites/default/files/2024-02/reel-charging-infra-for-trucks-2024.02.pdf